In a momentous move to empower prospective homeowners, the QLD government has recently unveiled a groundbreaking enhancement to the First Home Buyers Grant. This crucial financial support for first-time homebuyers has doubled from $15,000 to an impressive $30,000.

The revised grant seeks to provide substantial assistance to individuals purchasing or building their inaugural home, injecting vitality into the real estate market and offering financial relief to Queensland residents.

This enhanced grant is a transformative development for aspiring homeowners. It is specifically targeted at those acquiring a brand-new home or embarking on the exciting journey of constructing their first residence. The increased grant amount is applicable to homes with a maximum value of $750,000 (including land, build and variations), expanding the spectrum of eligibility and providing opportunities for a more extensive range of individuals and families.

To qualify for the increased grant, applicants must meet specific conditions, including being 18 years or older and being an Australian citizen or permanent resident (or applying with one). Additionally, the grant will only be approved for newly constructed homes that have never been occupied. These conditions underscore the government's commitment to stimulating the construction industry and fostering the development of new housing stock.

The emphasis on constructing new homes aligns with broader economic and environmental goals. By encouraging the construction of fresh, energy-efficient dwellings, the government is not only supporting the housing market, but also contributing to sustainability initiatives. This approach reflects a forward-thinking strategy that addresses both the immediate needs of citizens and the long-term well-being of the community.

Eligible applicants can start applying for the increased grant from the first week of January 2024. The scheme will run until 30 June 2025, providing a defined window of opportunity for individuals and families to take advantage of the doubled grant amount. The application process will likely involve submitting proof of eligibility, including age, citizenship, residency status and confirmation that the property is new and has never been lived in. The applicant must also move into the residence within 12 months of it being built and live there for a minimum period of 6 months.

The decision to double the First Home Buyers Grant is anticipated to have a profound impact on the Queensland economy. As more individuals and families enter the housing market, demand for new homes and construction services is expected to surge, potentially leading to job creation and benefiting local businesses.

Moreover, the infusion of funds into the real estate sector can stimulate related industries, such as home furnishings, appliances, and landscaping. This multiplier effect has the potential to generate a positive economic cycle, creating a win-win situation for both aspiring homeowners and the broader community.

Queensland’s decision to double the First Home Buyers Grant reflects a proactive approach to addressing the challenges faced by those looking to step onto the property ladder. By increasing the grant amount and focusing on new homes, the government aims to invigorate the housing market, promote economic growth, and fulfill the dreams of first-time homebuyers.

This announcement comes at a time when the importance of stable housing and financial support is more evident than ever. Aspiring homeowners now have a golden opportunity to turn their dreams into reality, thanks to the Queensland government's commitment to fostering a thriving and resilient community. Eligible applicants should mark their calendars and prepare to seize this unprecedented chance when applications open in the first week of January 2024. The scheme is set to run until 30th June 2025, providing a strategic window for individuals and families to embark on their homeownership journey with enhanced financial support.

For more information or if you have any questions around this information above, please reach out to our Queensland Director of Broking – Gemma Cuskelly – she is more than happy to help and has a passion in helping people achieve their property goals. Her email address is gemma.cuskelly@scarlettfinancial.com.au or you can follow her for more tips on Instagram @gemthebroker .

Article written by Gemma Cuskelly - Director of Scarlett Finance Queensland.

Over the past decade and a half, we have moved to a globalised, internet and smart phone-enabled, world. The market has become a globalised “winner takes all market”.

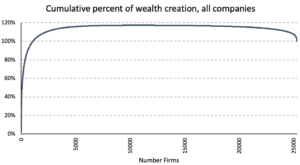

Power law probability distributions describe the situation where only a small percentage of a certain population produce most of the value. This type of probability distribution is also known as a Pareto Distribution. A common example is the “80-20” rule where 80% of the value is produced by 20% of the population. Even before the emergence of the internet, returns for global equity markets had been dominated by a small group of highly successful businesses. Most listed stocks produce unattractive long-term buy and hold returns. In a study of the returns produced by U.S. equities from 1926 to 2016, Hendrik Bessembinder (2018) finds an extremely narrow group of stocks drove all of the equity market returns. The top-performing 1,092 listed U.S. companies (or 4.31% of the total number of listed stocks during this time period) accounted for all of the wealth creation from investing in equities (i.e. excess equity returns relative to treasury bills). Bessembinder (2019) replicated this study across 42 countries over the 1990 to 2018 period and found the returns globally were even narrower where the best performing 811 firms (or 1.33%) accounted for all the net global wealth creation.

Stock market returns over the long term are not driven by most stocks but rather by a small number of structural growth businesses. The extraordinary returns from this small number of structural growth businesses result in the market’s return distribution having a positive skew rather than a normal bell curve shape. It is the compounding impact of high return structural growth businesses (“the winners”) that drive most stock market returns over the long term. Unless a long-term “buy and hold” investor can successfully select future structural growth companies, that is, the structural winners, and give them sufficient weight in their portfolio they will not produce excess returns.

Bessembinder (2018) provides evidence that long-term market returns are driven by a narrow number of long[1]term winners. The following charts clearly show how narrow the number of companies are that contribute to equity returns from 1926 to 2016 in the U.S. market. The super-abnormal returns of a select few businesses compensate for many losing or average performers:

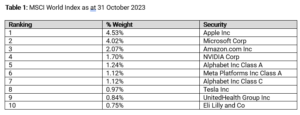

The creative destruction of capitalism means there are few winners. The world continues to migrate to a winner-takes-all model where average and below average companies continue to suffer from low industry demand growth and a structural decline in the relative strength of their value proposition to customers. We believe the return and performance profile of a select group of quality growth companies will persist. With the largest 5 companies in the MSCI World between 1.0% to 4.5% of the index each, some of these will become much larger components over the next decade. Market capitalisations of many trillions of dollars will become reality for the largest listed companies in the world over the next decade and beyond.

Value creation within capitalism is rarely linear and a long-term view is required. To maximise compound returns, we believe investors need to hold a small number of structural growth stocks for long time periods, generally many years to decades. We believe that true risk relates to permanent loss of capital or destruction of capital. Share price volatility is not risk. A sustainable business model is essential for earnings to compound over time. Investment should focus on qualitative elements such as value proposition, competitive advantage, strength of business model, recurring level of revenue and strength of balance sheet to ensure we have selected businesses that can survive permanently.

Conclusion

The fact that long-term cumulative equity returns are driven by a small number of exceptional equities does not mean the odds of success are necessarily low. Most experienced investors have some ability to recognise a few good investment ideas over the long term. By investing in a relatively concentrated number of high quality growth businesses, being patient and holding these businesses over the long term, investors can focus on their best investment ideas and benefit from the compounding growth in their value. This is an extremely powerful and effective approach to wealth creation. Over the long-term share prices follow organic sales growth per share and earnings per share growth. Hence stay disciplined and focused on the highest quality businesses – the structural winners.

The start of a new year is a great time to sit back, take stock of your financial situation and plan for the year ahead.

As accountants, we love End of Financial Year (EOFY), so put on your accountant hat and do a quick FINANCIAL EOFY REVIEW of your position, with some helpful hints from us.

We all know that keeping track of expenses and receipts is essential for getting the best tax outcome for ourselves and our businesses. So, let’s start the new year off on the right foot by getting organised and keeping track of those expenses and receipts. Excel is a tried-and-true option, but there are also a number of other software solutions that can make this process easier for you. If you are using Xero, take advantage of Hubdoc, a receipt processing software which is free with your Xero subscription. Hubdoc allows you to scan and upload your receipts directly to Xero, making it even easier to keep track of your receipts.

Getting the right structure for your business and investment assets is one of the most important investments you can make in your financial future. The right structure will deliver you the most optimal (read lowest) tax outcome this year and in future years to come.

The right structure will also ensure your assets are protected and that these hard fought for assets are not lost due to unforeseen circumstances, such as business failures, bankruptcy, or family separations.

For example:

The best way to choose the right structure for your needs is to speak to an accountant or financial planner. If you’re interest in talking about the best structure for you and your personal circumstances, please contact us.

We are talking about the essential, but not so fun types of insurances:

If you already have these types of policies in place and they have been reviewed recently, great work! You’re one step ahead of many people - full points!

if you have these types of policies through your superannuation fund but you haven’t reviewed them to make sure they are going to deliver the financial outcome you and your family need, it’s better than nothing but not ideal - half points!

If you don’t have any of these policies, you should get them in place as soon as possible.

These policies should evolve with you over the course of your life. For example:

Our Financial Planners are able to assist you with your personal insurance needs, even if it is just a general chat to sense check your cover. You will never regret looking into this and ensuring you and your family are taken care of.

A good business can be a valuable asset, but in the event of death or illness of the owners who are instrumental to the operation of the business, the value can quickly be lost, or it can be very hard to extract in a sale situation.

To protect the value of the business, business owners can take out life insurance, TPD insurance and Key Person insurance over owners and key personal to protect the value of the business.

If you have such policies in place, that’s great! But like all things, they need to be reviewed regularly to ensure they are adequate for the current businesses’ needs.

If you are interested in talking about your existing insurances or putting them in place, please contact us.

Let’s be honest, no one likes to think about death, which is very apparent to us as we see too many people who either don’t have a will or have not renewed their estate plan for many years.

You should consider looking into your estate planning if:

Similarly, if you have recently started a business and/or established a company or trust that you control, it is imperative that these changes to your financial structure are dealt with in your will, so it’s time for an update!

If this is something that is keeping you up at night (or maybe it should be), we can refer you to an estate planning lawyer to put in place the appropriate measures to give you peace of mind that your loved ones will be looked after if the worst was to happen to you.

Interest rates have been increasing significantly over the recent months. We are still seeing too many people paying more interest than they should be. This is known as the ‘bank loyalty tax’, which is a term we use to describe the extra interest you pay when you stay with the same lender, even though there may be better rates available elsewhere. We often see people paying up to 1% more than what otherwise may be available.

There are a couple of ways we can help:

If you’re interested in learning more about how we can help you with your loan interest rates, please contact us.

Like everything else it seems at the moment, insurance premiums are skyrocketing. Now is a good a time as any to review your insurance policies to ensure you are not paying more than you need to, and most importantly ensuring you have sufficient cover over your assets if something was to go wrong.

Buying a first home is a monumental milestone in anyone's life. It marks a significant step towards financial independence and stability. However, the process of finding the perfect home can be both exciting and challenging. From house-hunting to negotiating offers, it demands dedication, patience and persistence. Here are our top three tips to remember when embarking on the journey of purchasing your first home.

Tip #1 - Get Pre-Approved and Define Your Priorities

Before diving into the real estate market, be sure to seek pre-approval from a trusted broker and then take the time to sit down and define your priorities. Pre-approval is a very important step in property purchase. It allows you to work within a budget and gives you greater negotiating power when it comes time to make an offer.

Creating a clear list of what you want and need in your new home will help you stay focused during the search. Consider factors like location, size, layout, amenities, and budget. Ask yourself questions like:

Location. Is it important to be close to work, family, or certain amenities? What kind of neighbourhood do you envision yourself living in?

Size & Layout. How many bedrooms and bathrooms do you need? Are you looking for an open floor plan or more traditional segmented spaces?

Amenities. What features are essential to you? This could include a backyard, a garage, or specific appliances.

Budget. By obtaining pre-approval, you are determining how much you can afford to spend on your first home. Remember to factor in additional costs like property taxes, conveyancing fees, insurance, and potential renovations.

Having a clear set of priorities will make your house-hunting journey more efficient and less overwhelming.

Tip #2 - Work with a Trusted Real Estate Agent or Buyers Agent

Navigating the complex world of real estate can be intimidating, especially for first time buyers. Enlisting the help of a trusted and experienced real estate or buyers agent can make a world of difference. A skilled agent will possess a deep understanding of the local market, have access to a broader range of listings, and be adept at negotiating on your behalf.

Here are some tips to find the right real estate agent:

Referrals. Seek recommendations from friends, family, or colleagues who have recently bought a home. They can share their experiences and refer you to a reliable agent.

Research. Look for agents with a strong track record and positive reviews online. Read testimonials from previous clients to gauge their satisfaction.

Compatibility. Meet with potential agents to ensure your personalities and communication styles align. You'll be working closely with this person, so a good fit is crucial.

A knowledgeable real estate or buyers agent will streamline the home-buying process, providing valuable insights and assistance every step of the way.

Tip #3 - Stay Patient & Flexible

In a competitive real estate market, finding the perfect home that meets all your criteria may take time. It's essential to stay patient and be prepared for some compromises. Understand that you might not find your dream home immediately, but that doesn't mean you should settle for something that doesn't fit your needs entirely.

Be open to exploring different neighbourhoods and property types. Sometimes, the perfect home may not check all the boxes on your list but could have great potential with a few renovations or modifications.

Moreover, the negotiation process might require some back-and-forth with the seller. Don't rush into decisions, and always consult with your broker and/or real estate agent before making an offer. A little persistence and flexibility can lead you to a home that truly feels like the right fit.

Written by Gemma Cuskelly.

We’re thrilled to announce that we’ve opened a new permanent office on the Gold Coast. The office is located at 11A/1134 Gold Coast Highway, Palm Beach.

The new office is led by Nathan Nash, a founding Director of Scarlett Financial and Private Wealth Adviser with over 20 years’ experience in the financial services industry.

This is a major milestone for our company, and we’re excited to see what the future holds for us. We’re already seeing strong growth in our Gold Coast office, and we’re confident that this trend will continue.

Thank you for your continued support!

Our financial planning team recently caught up with strategists from JP Morgan to discuss the outlook for the remainder of the year given the current economic climate.

Key Points from the Meeting

At the start of the year, it was expected that 2023 would be more challenging for central bankers around the world. Instead of raising rates aggressively to cool inflation against a strong economic backdrop, they now need to balance their monetary policy between stubborn inflation and a greater risk of economic recession and financial sector shocks.

A sign that rate rises will continue to slow, and perhaps start coming back down, is that the cash rates are now hitting their peak predicted policy rates from the forecasts back in March. Additionally, there are growing signs that the economy is slowing with lending tightening and becoming more difficult.

The unemployment rate continues to be solid and household spending is still in good shape. However, a reduction in corporate spending and a weaker housing market places pressure on the Fed to start bringing rates down, even if inflation is slow to come down.

JPMorgan analysts expect rate cuts to start becoming evident around September for the US market. This expectation could be built upon previous rate cycles where the average period of the last hike to the first cut is around 6 months. That being said, historical precedents may be less applicable now with inflation still being the top priority for the Fed.

In summary, it can be expected that rates will start to wind back down towards the end of the year, and it will likely result in weaker growth. From an investment perspective, this means longer-term fixed income products, high quality stocks and defensive sectors are expected to outperform after a few years of poorer returns.

Written by Jackie Crane.

The NSW First Home Buyer Choice kicked in on 12 November, offering first home buyers the opportunity to choose between paying a smaller annual property fee or a large upfront stamp duty on their first property, up to $1.5 million.

While the policy becomes fully operational on 16 January 2023, eligible first home buyers purchasing a property from now until 15 January 2023 will be able to switch to the annual property tax and have their stamp duty refunded.

Here’s a link to a great article on the scheme to help you understand what might be best for you: Stamp Duty vs Land Tax: First Home Buyer Choice Explained | Canstar

As always – the preference here will depend on your circumstances.

There’s a couple of considerations: Firstly – what’s the overall best financial outcome; and Secondly - if maximizing your purchase price is the priority which option better allows you to do this.

In most cases - based on how long first home buyers stay in their first property, the size of the dwelling and therefore associated land value (units / town houses etc) - the property tax will work out as a better financial option. NSW Treasury expects that up to two-thirds of first home buyers will choose to pay a smaller annual property fee rather than forking out for stamp duty upfront, especially those spending between $800,000 and $1.5 million who plan to sell their property within 10 years of purchase.

However, the property tax expense also needs to be factored into your annual budgeting as it is another ‘liability’ that will impact your loan servicing capacity and therefore maximum borrowing power. Some first home buyers are limited on their maximum purchase price based on their savings and deposit, whilst others are limited by income and serviceability. While this significantly assists those restricted by their savings or overall deposit, it will not be helpful for those restricted by income as this annual tax will further reduce their borrowing power.

As always – you should speak to mortgage professional who can help you decide what might be best for you before deciding which way to go.

Please reach out to us should you have any questions or can assist in anyway.

Insurance is designed to restore your home or business to the condition it was in before an insured loss without financial penalty. Regardless of what amount your asset was originally bought for and how much you believe it could be worth, the sum insured must either be equivalent to the current replacement value or the current market value, depending on the type of policy you have.

Underinsurance occurs when the insured value of your home or business assets is less than the rebuild or replacement costs. As well as not receiving enough money to cover the cost of your loss, if you significantly underinsure your home, contents, or business assets, the insurer may have the right to reduce the claim payout by the same percentage/amount as the underinsurance.

As a home or business owner, it is your responsibility to value your assets, whether that is by using an online calculator or a certified property valuer. Although as your insurance advisor we cannot give advice around the sums insured for a building, we can advise clients about the risks of underinsurance, question if they have done a recent review of the rebuild/ replacement value and if the recent rises of the cost of building materials have been considered.

It is important to consider that the dollar is being devalued by inflation, which is also possibly limiting the coverage your insurance offers. Inflation rates are at the highest they have been in a generation. Pandemic lockdowns, supply chain delays, disruptions in the energy supply, and a lack of workers have increased the value of various commodities and extended the completion dates for services ranging from infrastructure development to legal proceedings. When these price surges are taken into consideration, replacement values for tangible assets, including fleet cars, plant and equipment, items in transit, and property, may be significantly higher than their insured estimates.

The potential impacts of being underinsured can be financially devastating. If your home experiences a total loss and you are underinsured, you will be responsible for paying the shortfall to rebuild the property.

Below is an example of underinsurance and the potential shortfall in the event of a loss:

Some important tips to avoid underinsurance are to assess your policy and sums insured frequently, value your assets correctly and seek professional advice from your broker.

As your insurance advisor, we can assist with: