Nathan Nash is a Private Wealth Advisor of Scarlett Wealth and provides strategic wealth creation and wealth preservation strategies. Nathan provides strategies that combine investment options based on an individual's personal situation and the market opportunity.

A founding Director of Scarlett Financial, Nathan has over 20 years experience in the financial services industry. He has extensive knowledge in advising wealth accumulators and small business owners on how to build financial security and maximise lifestyle opportunities through to retirement.

Nathan’s role involves two main parts:

Financial Position Maximisation

To provide professional advice in maximising your current financial position through diversified investment construction, tax effective asset structuring, and strategic planning of personal resources.

Long Term Financial Planning & Strategy

To provide a strategic long-term plan to best meet your personal goals as efficiently and securely over time. To maximise the success of long-term planning we provide ongoing strategic planning, investment advice, performance and goal benchmarking.

My Services – Financial Planning

Brisbane

We have been working with Nathan of Scarlett Financial for over 15 years. We have complete faith that he always has our best interests at heart and his results have proved his work ethic. He continually takes in our overall situation to give advice tailored to our particular needs and lifestyle choices.

Nathan and the team were there to advise me through my husband's deceased estate and have since been providing me with reassurance and security. The relationship has always been friendly and personal, no questions too silly, easy to understand information and ample reporting. I tell Nathan he is not allowed to retire.

The Scarlett Advisory team are extremely professional and always available to assist me. I know I can rely on the team to provide me with relevant and timely advice that is specific to both my business and industry. They constantly go above and beyond their roles to guide me in running my business, through their industry-specialised knowledge within the medical field.

Nathan Nash has an incredible ability to make even the most complicated compliance issues digestible. He has been providing our family with sound financial planning advice for over ten years.

Welcome to your one-stop hub for the latest happenings in the world of finance. Keep up to date by reading my articles below, my first article is coming soon.

We have been working with Nathan of Scarlett Financial for over 15 years. We have complete faith that he always has our best interests at heart and his results have proved his work ethic. He continually takes in our overall situation to give advice tailored to our particular needs and lifestyle choices. We can’t recommend Nathan’s integrity, professionalism, and friendly nature highly enough to anyone looking for a trustworthy financial advisor.

Nathan Nash and Scarlett Financial have been managing my SMSF and assisting with my personal budgeting requirements for over a decade. Nathan and the team were there to advise me through my husband's deceased estate and have since been providing me with reassurance and security. The relationship has always been friendly and personal, no questions too silly, easy to understand information and ample reporting. I tell Nathan he is not allowed to retire.

The Scarlett Advisory team are extremely professional and always available to assist me. I know I can rely on the team to provide me with relevant and timely advice that is specific to both my business and industry. They constantly go above and beyond their roles to guide me in running my business, through their industry-specialised knowledge within the medical field.

As well as being exceptional at what they do, the team at Scarlett Financial possess a genuine desire to develop and maintain a relationship on a personal level. (Something which shows that the team are not just about charging fees and seeing me once a year to talk about my taxes and obligations to the ATO.) They truly care about me and my business.

I highly recommend the Scarlett Advisory team to anyone wanting to improve their business profitability and desire to achieve a successful work/life balance.

Nathan Nash has an incredible ability to make even the most complicated compliance issues digestible. He has been providing our family with sound financial planning advice for over ten years.

Nathan is personable, approachable and an all-round genuine guy. He always has time for us and provides a personalised approach which is a welcome relief to our otherwise extremely busy schedule.

Home owners have been battling rising interest rates for over a year and a half now. But a new report reveals the important step some savvy borrowers are taking to rein in higher rates and swap “oh no!” for “ho, ho, ho!”.

It’s no secret that refinancing has the potential to slice a big chunk off your monthly loan repayments.

And according to Canstar, 1 in 10 mortgage holders chased a better deal in 2023 and switched to a new lender to save on their repayments.

But what’s surprising to us is that 9 in 10 didn’t.

So what’s holding them back? Let’s dive in.

To be fair, many home owners have been on the front foot this year.

According to Canstar, 1 in 5 home owners with a mortgage have negotiated a better rate with their current lender – which is great news.

Having a chat with your bank can be a fuss-free way to save, especially if they come to the party with a rate discount.

A further 14% of home owners say they have tried to switch to another lender but weren’t able to do so because they didn’t have enough equity, or didn’t meet the new lender’s requirements.

That’s why it pays to speak with us before talking to a lender.

We have in-depth knowledge of different banks’ lending criteria, so we know which lenders are likely to give you the green light for a better deal.

The thing is, there are plenty of home owners who have just copped rising rates without taking action.

As Canstar puts it: “Too many borrowers remain complacent even in the face of rising repayment costs”.

The scary thing is, half (49%) of Australia’s home owners with a mortgage don’t intend to change lenders at all.

Some believe they have a good interest rate. But as many as 1 in 5 think refinancing is too hard.

Let’s sort some facts from fiction.

First up, it’s great if you think you are paying a competitive interest rate. The key is to know for sure.

Right now, variable home loan rates are anywhere from 5.69% (very rare) through to 9%-plus.

With that sort of range, there’s plenty of scope to save, especially as lenders often make lower rates available to new customers.

There is an easy way to know if you’ve got a good rate: pick up the phone and call us.

And if you’re worried that refinancing is hard work, rest assured that we’ll do the bulk of the leg work for you.

We’ll sort through hundreds of home loan options to find the loan that’s right for your needs. We’ll also make the paperwork easy, liaise with your old lender, and your new bank. Simple.

So if you’re keen to find out if you can do better with your home loan these summer holidays, give us a call and we’ll help you put your best foot forward going into 2024.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

If buying a home is at the top of your wish list for 2024, don’t miss our rundown on how the property market has fared in 2023 – and why the new year is shaping up as potentially another big year for real estate.

As we turn the page on 2023, let’s take a quick rear mirror look on how home values moved over the past 12 months.

In a year that saw five official rate hikes, and a cost of living squeeze thanks to high inflation, home prices still jumped by 7% nationally.

Several cities eclipsed those gains, with double-digit price growth in Sydney (up 10.2%), Brisbane (10.7%) and Perth (13.5%).

But it wasn’t just price growth that took everyone by surprise.

The speed of home sales was also astonishing, with plenty of suburbs in Perth, Sydney, Brisbane and Melbourne selling houses in as little as eight to 25 days on average.

Well, higher interest rates are starting to take a little heat out of the market.

According to CoreLogic, home values across Australia rose 0.6% in November – the smallest monthly gain since early 2023.

But here’s the rub.

The factors that pushed prices higher in 2023 are still in place, and plenty of experts are tipping house prices will keep rising in the new year.

Three main drivers look set to support house price growth in 2024, including:

1. Strong population growth: Population growth is rebounding strongly, driven by high immigration levels. More people generally means more demand for housing.

If you’re not convinced, a recent Domain report says “unprecedented” population growth will exert “extraordinary upward price pressure” on the property market.

2. A housing undersupply: On the supply side, we’re just not building enough new homes.

Australia’s housing shortage made headlines through 2023, and it doesn’t look like it’ll get better any time soon. Building approvals for new homes are reported to be well below average levels.

3. A rental market that’s as tight as a drum: Anyone looking for a rental can face an uphill battle. Vacancy rates are at record lows, making rental conditions tough.

This could encourage more people to buy a place of their own through one of the government’s low deposit buying schemes.

The First Home Guarantee scheme for instance, lets first home buyers get into the market with just a 5% deposit and zero lenders mortgage insurance.

Most experts are tipping house prices will keep rising in 2024 though maybe not at the breakneck speed seen nationally in 2023.

That said, price growth won’t be anything to sneeze at.

Domain is forecasting house prices to jump 5-7% nationally, and in each capital city by:

– 7-9% in Sydney

– 2-4% in Melbourne

– 7-8% in Brisbane

– 6-7% in Perth

– 7-8% in Adelaide

– 3-5% in Canberra

– 2-4% in Hobart

The bottom line is that we could be facing another bumper year of price growth in 2024, and if buying is on your radar, it may be worth trying to buy sooner rather than later to potentially avoid paying more.

So call us today to get the ball rolling on a home loan that helps you achieve your new year property goals sooner.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

First home buyers with a small deposit now have an even wider range of lenders to choose from. We reveal the latest banks to join the 5% deposit scheme that’s helping more buyers get into the market sooner.

First home buyers have just received an early Christmas gift, of sorts, with an uptick in the number of lenders that have signed up to the Home Guarantee Scheme (HGS).

Three Westpac brands, St.George, Bank of Melbourne and BankSA, have added their names to the list of lenders available to first home buyers under the HGS.

If you’re not familiar with the HGS, it gives first home buyers an opportunity to buy a place of their own with as little as a 5% deposit (and no lenders mortgage insurance) through the First Home Guarantee or Regional First Home Buyer Guarantee.

First home buyers aren’t the only ones to benefit. The HGS also includes the Family Home Guarantee, which allows solo parents to buy a home with just a 2% deposit.

According to Housing Australia, which runs the HGS, first home buyers can now choose from 33 lenders participating in the scheme.

This includes most of the big banks (ANZ has not signed up) plus a generous variety of small banks, credit unions and non-bank lenders.

The extra sweetener is that more lenders can boost competition, which potentially encourages banks to keep their interest rates low for first home buyers.

Saving a deposit is often the key barrier for first home buyers. And when home prices and cost of living are rising, it can seem like the goal posts are constantly moving out of reach.

The beauty of the HGS is that it lets first home buyers jump into the property market about four years earlier (on average) than they normally would.

So, it’s no surprise that last financial year one-in-three first home buyers purchased with the help of the HGS.

Better yet, new data from Housing Australia shows that first buyers who have tapped into the scheme are now sitting on $82,000 in home equity, on average.

It’s a great result, especially when you consider that the average first home deposit across the scheme was just $35,200 in 2020, rising to $36,400 in mid-2023.

Compare that to the average deposit of $159,000 across the broader first-home buyer market, and it’s easy to see how the 5% deposit scheme gives first-home buyers a valuable leg-up into the market sooner.

With more than 40 lenders offering 5% deposit home loans under the HGS, the challenge can be choosing the loan and lender that’s right for your needs (or finding one that will take you on if your application is a bit touch and go, or if you’ve just started your own business in recent years).

The simple solution is to give us a call.

We can explain whether you’re eligible for the low-deposit scheme, and answer any questions you may have.

We’ll also take the time to understand your needs, so you can be confident that the lenders and loan products we put forward to you are a good fit.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

In a momentous move to empower prospective homeowners, the QLD government has recently unveiled a groundbreaking enhancement to the First Home Buyers Grant. This crucial financial support for first-time homebuyers has doubled from $15,000 to an impressive $30,000.

The revised grant seeks to provide substantial assistance to individuals purchasing or building their inaugural home, injecting vitality into the real estate market and offering financial relief to Queensland residents.

This enhanced grant is a transformative development for aspiring homeowners. It is specifically targeted at those acquiring a brand-new home or embarking on the exciting journey of constructing their first residence. The increased grant amount is applicable to homes with a maximum value of $750,000 (including land, build and variations), expanding the spectrum of eligibility and providing opportunities for a more extensive range of individuals and families.

To qualify for the increased grant, applicants must meet specific conditions, including being 18 years or older and being an Australian citizen or permanent resident (or applying with one). Additionally, the grant will only be approved for newly constructed homes that have never been occupied. These conditions underscore the government's commitment to stimulating the construction industry and fostering the development of new housing stock.

The emphasis on constructing new homes aligns with broader economic and environmental goals. By encouraging the construction of fresh, energy-efficient dwellings, the government is not only supporting the housing market, but also contributing to sustainability initiatives. This approach reflects a forward-thinking strategy that addresses both the immediate needs of citizens and the long-term well-being of the community.

Eligible applicants can start applying for the increased grant from the first week of January 2024. The scheme will run until 30 June 2025, providing a defined window of opportunity for individuals and families to take advantage of the doubled grant amount. The application process will likely involve submitting proof of eligibility, including age, citizenship, residency status and confirmation that the property is new and has never been lived in. The applicant must also move into the residence within 12 months of it being built and live there for a minimum period of 6 months.

The decision to double the First Home Buyers Grant is anticipated to have a profound impact on the Queensland economy. As more individuals and families enter the housing market, demand for new homes and construction services is expected to surge, potentially leading to job creation and benefiting local businesses.

Moreover, the infusion of funds into the real estate sector can stimulate related industries, such as home furnishings, appliances, and landscaping. This multiplier effect has the potential to generate a positive economic cycle, creating a win-win situation for both aspiring homeowners and the broader community.

Queensland’s decision to double the First Home Buyers Grant reflects a proactive approach to addressing the challenges faced by those looking to step onto the property ladder. By increasing the grant amount and focusing on new homes, the government aims to invigorate the housing market, promote economic growth, and fulfill the dreams of first-time homebuyers.

This announcement comes at a time when the importance of stable housing and financial support is more evident than ever. Aspiring homeowners now have a golden opportunity to turn their dreams into reality, thanks to the Queensland government's commitment to fostering a thriving and resilient community. Eligible applicants should mark their calendars and prepare to seize this unprecedented chance when applications open in the first week of January 2024. The scheme is set to run until 30th June 2025, providing a strategic window for individuals and families to embark on their homeownership journey with enhanced financial support.

For more information or if you have any questions around this information above, please reach out to our Queensland Director of Broking – Gemma Cuskelly – she is more than happy to help and has a passion in helping people achieve their property goals. Her email address is gemma.cuskelly@www.scarlettfinancial.com.au or you can follow her for more tips on Instagram @gemthebroker .

Article written by Gemma Cuskelly - Director of Scarlett Finance Queensland.

It may be called the silly season but a few smart strategies could help you enjoy the festive season this year without missing a beat on your home loan. Check out our tips to share the Christmas cheer this year without breaking the bank.

Store shelves are starting to be lined with tinsel, ‘Santa stop here’ signs are popping up around the neighbourhood, and chances are you’re beginning to hum a few bars of Jingle Bells.

Yes, Christmas is just around the corner, and now’s the time to plan for what can be a pricey time of year.

After 13 rate hikes in close succession, plenty of homeowners are feeling the squeeze of higher home loan repayments.

The good news is that you (hopefully) won’t have to cancel Christmas this year. Below are three clever hacks that could help you manage your mortgage over the festive season.

Plan ahead by listing all the fixed expenses you’ll face in December such as utilities, your home loan, car loan, and credit card repayments, as well as less frequent bills such as council rates that may fall due before Christmas.

Add up the total to know how much you need to set aside. It’s a good idea to try and prioritise these bills over seasonal spending.

Next, draft up a Christmas spending budget that allocates money to gifts, food, drinks and decorations.

Finetune your budget based on your ability to pay, bearing in mind the upcoming costs you identified in the bill list.

If things are looking tight this year, consider opting for Secret Santa instead of everyone buying everyone a present.

It can help make the giving experience more personal and is definitely gentler on the hip pocket.

Websites like elfster.com can help keep it anonymous and straightforward for everyone.

It can be tempting to pay for Christmas purchases with a credit card or buy now, pay later. But these options can just mean kicking the can down the road until January when payments fall due.

It’s also worth noting that late payments on either option could affect your credit score for any future home loan applications.

So where possible, consider reaching for your debit card for festive purchases. It’s hard to get into too much trouble when you pay using your own money.

Christmas is the season of giving, so why don’t we hit up your lender for the gift of a lower interest rate?

Reserve Bank data shows there is still a gap between the rates on new versus established loans.

If you took out your loan through us, get in touch and we can either reach out to your lender on your behalf for a discount or, if they don’t come to the party, help you explore your refinancing options with another lender.

It’s easy to get swept up in seasonal good cheer. But it can sometimes be important not to get too carried away with Christmas spending.

If you plan to refinance your home loan or purchase a house in 2024, a lender will likely look at your spending patterns over the past few months.

Hamming up your purchases in December can bump up your average living costs, and if you go way over the top, potentially see you knocked back for a new loan in the new year.

Want more tips to manage your mortgage over the holiday season? Call us today for more festive saving strategies.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

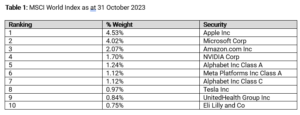

Over the past decade and a half, we have moved to a globalised, internet and smart phone-enabled, world. The market has become a globalised “winner takes all market”.

Power law probability distributions describe the situation where only a small percentage of a certain population produce most of the value. This type of probability distribution is also known as a Pareto Distribution. A common example is the “80-20” rule where 80% of the value is produced by 20% of the population. Even before the emergence of the internet, returns for global equity markets had been dominated by a small group of highly successful businesses. Most listed stocks produce unattractive long-term buy and hold returns. In a study of the returns produced by U.S. equities from 1926 to 2016, Hendrik Bessembinder (2018) finds an extremely narrow group of stocks drove all of the equity market returns. The top-performing 1,092 listed U.S. companies (or 4.31% of the total number of listed stocks during this time period) accounted for all of the wealth creation from investing in equities (i.e. excess equity returns relative to treasury bills). Bessembinder (2019) replicated this study across 42 countries over the 1990 to 2018 period and found the returns globally were even narrower where the best performing 811 firms (or 1.33%) accounted for all the net global wealth creation.

Stock market returns over the long term are not driven by most stocks but rather by a small number of structural growth businesses. The extraordinary returns from this small number of structural growth businesses result in the market’s return distribution having a positive skew rather than a normal bell curve shape. It is the compounding impact of high return structural growth businesses (“the winners”) that drive most stock market returns over the long term. Unless a long-term “buy and hold” investor can successfully select future structural growth companies, that is, the structural winners, and give them sufficient weight in their portfolio they will not produce excess returns.

Bessembinder (2018) provides evidence that long-term market returns are driven by a narrow number of long[1]term winners. The following charts clearly show how narrow the number of companies are that contribute to equity returns from 1926 to 2016 in the U.S. market. The super-abnormal returns of a select few businesses compensate for many losing or average performers:

The creative destruction of capitalism means there are few winners. The world continues to migrate to a winner-takes-all model where average and below average companies continue to suffer from low industry demand growth and a structural decline in the relative strength of their value proposition to customers. We believe the return and performance profile of a select group of quality growth companies will persist. With the largest 5 companies in the MSCI World between 1.0% to 4.5% of the index each, some of these will become much larger components over the next decade. Market capitalisations of many trillions of dollars will become reality for the largest listed companies in the world over the next decade and beyond.

Value creation within capitalism is rarely linear and a long-term view is required. To maximise compound returns, we believe investors need to hold a small number of structural growth stocks for long time periods, generally many years to decades. We believe that true risk relates to permanent loss of capital or destruction of capital. Share price volatility is not risk. A sustainable business model is essential for earnings to compound over time. Investment should focus on qualitative elements such as value proposition, competitive advantage, strength of business model, recurring level of revenue and strength of balance sheet to ensure we have selected businesses that can survive permanently.

Conclusion

The fact that long-term cumulative equity returns are driven by a small number of exceptional equities does not mean the odds of success are necessarily low. Most experienced investors have some ability to recognise a few good investment ideas over the long term. By investing in a relatively concentrated number of high quality growth businesses, being patient and holding these businesses over the long term, investors can focus on their best investment ideas and benefit from the compounding growth in their value. This is an extremely powerful and effective approach to wealth creation. Over the long-term share prices follow organic sales growth per share and earnings per share growth. Hence stay disciplined and focused on the highest quality businesses – the structural winners.

If the November rate hike will seriously stretch your finances, one potential solution may be to extend your loan term. It can ease the hip pocket pain by lowering monthly repayments. But taking more time to pay off your mortgage can come with hidden downsides. Here’s what to weigh up.

Will the RBA’s latest 0.25% cash rate rise squeeze you financially? (not to mention the other 12 rate hikes!)

The majority of lenders lost no time increasing their variable home loan rates following the Reserve Bank of Australia’s 0.25% Melbourne Cup Day rate rise.

According to Mozo, the 13th rate hike since May 2022 has pushed up the average variable rate to 6.62%.

On a $500,000 variable rate home loan payable over 25 years, the latest 0.25% rate hike can see monthly repayments jump by $78.

For homeowners who didn’t have much fat left to cut from their budget, those extra dollars can be hard to find.

One potential strategy that may help to lower repayments is to stretch out your loan term.

If you have a 25-year loan, your lender may give you the option to extend for up to five more years, possibly pushing out the term to 30 years.

If you get the green light, this kind of reset can significantly lower your monthly repayments.

On the $500,000 mortgage we looked at earlier, moving from a 25-year loan to a 30-year loan could cut monthly repayments by around $214 – even after allowing for the November rate hike.

There’s a lot to love about the prospect of slashing a couple of hundred bucks off your loan repayments each month, especially as we head into the festive season.

But pushing out your loan term can come with a hidden cost.

Taking longer to pay down your loan means you’re also paying interest for longer. And while your repayments can decrease, the long-term interest cost can skyrocket.

Stretching a $500,000 loan from 25 to 30 years could mean paying a whopping $128,000 more in total interest.

It’s worth keeping in mind though that those extra interest repayments aren’t a given.

You may be able to close the gap and cut down the interest cost by either making extra repayments in the future, loading up an offset account, or paying off the loan early (if, for example, you receive a lump sum inheritance).

So the upshot is that stretching your loan term can be a short-term fix now, but you’ll have to weigh up the costs against the benefits, not to mention whether you think you’ll be in a better financial position later down the track to pay down the loan quicker (and thus reduce the interest payments).

Along with exploring extending the length of your loan, we could also help you look into other solutions to ease the pain of higher rates.

Options that may be available with your lender include:

– temporarily lowering your loan repayments;

– deferring repayments for a while; or

– shifting you to interest-only payments for a set period.

The common thread is that the earlier you reach out for assistance, the sooner we may be able to help you get some financial relief.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

The Reserve Bank of Australia (RBA) has increased the official cash rate by 25 basis points, taking it to 4.35%. So just how much will this year’s Melbourne Cup day rate hike increase your monthly repayments?

Some more tough news for mortgage holders around the country today.

Despite the official cash rate being on hold since June (and many hoping it would stay that way), the RBA has decided to press ahead with a second consecutive Melbourne Cup day rate rise in an attempt to rein in inflation.

This means we’ve now had 13 hikes rise in 18 months since 1 May 2022, and it takes the official cash rate to its highest level since November 2011.

It also happens to be the first rate hike under new RBA Governor Michele Bullock, who commenced in the role in September.

Governor Bullock said while inflation in Australia had passed its peak, it was still too high and was proving more persistent than expected a few months ago.

“While goods price inflation has eased further, the prices of many services are continuing to rise briskly,” she said.

“While the central forecast is for CPI inflation to continue to decline, progress looks to be slower than earlier expected.”

Governor Bullock added the RBA Board judged an increase in interest rates was warranted today to be more assured that inflation would return to target in a reasonable timeframe.

“If high inflation were to become entrenched in people’s expectations, it would be much more costly to reduce later, involving even higher interest rates and a larger rise in unemployment,” she said.

If you’re on a variable-rate home loan, the banks will likely be increasing the interest rate on it very shortly.

For an owner-occupier with a 25-year loan of $500,000 paying principal and interest, this month’s 25 basis point increase means your monthly repayments could go up by about $76 a month.

That’s an extra $1,211 a month on your mortgage compared to 1 May 2022.

If you have a $750,000 loan, repayments will likely increase by about $114 a month, up $1,816 from 1 May 2022.

Meanwhile, a $1 million loan will increase by about $152 a month, up about $2,422 from 1 May 2022.

Are you feeling the pinch? You’re not alone. Many households around the country are feeling the effects of 14 rate hikes in 18 months.

There are also lots of people on fixed-rate home loans wondering what options will be available to them once their fixed-rate period ends.

Some options we can help you explore include refinancing (which could mean increasing the length of your loan and decreasing monthly repayments), debt consolidation, or building up a cash buffer in an offset account.

So if you’re worried about how you might meet your repayments going forward, give us a call today. The earlier we sit down with you and help you make a plan, the better we can help you manage your mortgage moving forward.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Mortgage brokers have notched up a new personal best, with seven out of every 10 new mortgages settled thanks to their help! It’s a sure sign that mortgage brokers are delivering the goods when it comes to helping Australians move into their dream homes.

In the nine months to 31 March 2023 (while interest rates were rising), mortgage brokers helped settle more than 70% of all new residential home loans, according to the latest data from the MFAA.

It’s the first time ever that brokers have helped settle more than 70% of home loans over a three-month-plus period.

For context, just two years earlier brokers were helping settle between 50-60% of new home loans.

For starters, it looks like word is getting out about how much help we can provide when it comes to giving you an informed choice with your home loan.

And in this environment of higher interest rates, it’s important to be sure your home loan offers value.

With a wide network of lenders – including big banks, small banks and non-banks – brokers are well-placed to help you choose the loan that’s right for you.

It doesn’t end there, though. Here are five more reasons why Australians are turning to brokers for help.

There are hundreds of home loans to choose from. But who’s got the time to find a loan that suits your needs?

Your broker does.

Better still, your broker does a lot of the legwork, sorting the paperwork and supporting your loan application right through to settlement.

That lets you sit back, relax, and focus on moving into your new home.

You’re busy, right? That’s why brokers offer flexible appointment times.

Want to chat after hours? No problemo.

Prefer to chat online rather than face-to-face? Can do.

It may seem like a minor benefit, but the flexibility brokers offer is a big deal when you’re flat out with work, family, or just busy house hunting.

Brokers provide clear details to help you make informed decisions.

From your borrowing power, to how much of a deposit you really need, and what your loan repayments will be under various scenarios, we’ll crunch the numbers based on your unique situation.

It takes the guesswork out of buying a home and lets you plan ahead.

It often comes as a surprise that a broker’s home loan help comes at no cost to their clients. That’s because brokers are paid a commission by lenders.

Rest assured though that unlike the banks, we’re (happily) bound by a best interests duty that means we’ll always put your best interests first.

So while banks and digital lenders might try to tempt you with cashback offers for loan products that may not really be in your best interests (due to fees, high interest rates, and other undesirable loan terms), we’ll only ever try to match you up with lenders and loans that are in your best interests.

Chances are you’ll have your home loan for quite a few years.

We’ll be with you along the way to help make sure your home loan continues to be the right option for you, no matter how your life changes.

So call us today to see why more Australians than ever are partnering with a broker.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

No matter whether you’re in the market for a home or an investment property, it makes financial sense to buy in an area where values are tipped to rise. But where to look? Today we’ll unveil the Australian cities where population growth is tipped to turbo-charge the property market.

One of the biggest drivers of property price rises right now is … drumroll … population growth, according to PropTrack.

Let’s take a look at the cities more people are expected to call home.

During the height of the COVID-19 pandemic, Australians were flocking to regional areas.

The population of regional Australia grew by 70,900 people during 2020-21 – the first time in over 40 years that the regions outpaced capital cities.

However, the COVID-inspired rush to the regions is reportedly over.

Despite the new work-from-home trend, the reopening of borders is seeing a return to urban living.

According to property exchange platform PEXA, this will see two-thirds of Australia’s population growth concentrated in four cities over the next two decades.

PEXA is predicting population growth of 7.4 million between now and 2041.

That’s a lot of people looking for a place to live.

It’s not just about net migration to Australia, either.

Regional dwellers, especially younger people, are expected to head to urban areas, attracted by the availability of study and work opportunities.

The upshot is that two million new homes will be required over the next 18 years, and 67% of population growth will be concentrated in Sydney, Melbourne, Brisbane and Perth.

The stats are astonishing.

PEXA says the four hotspot cities require vast numbers of new homes:

– 723,000 in Melbourne (that’s 40,000 new homes per year, or 772 per week);

– 582,000 in Sydney;

– 381,000 in Brisbane; and

– 334,000 in Perth.

Adelaide meanwhile is predicted to need at least another 141,000 dwellings between now and 2046.

For starters, increased demand on this scale is expected to continue to push up property prices unless supply can increase at a similar pace.

Despite higher interest rates, already we have seen values rise in all of these four cities over the past 12 months.

CoreLogic says property prices have soared 7.3% in Sydney over the past year, 5.0% in Brisbane, a whopping 8.8% in Perth, and a comparatively modest 1.5% in Melbourne (and 5.0% in Adelaide).

So if you own property in these cities, you could be sitting on more equity than you realise – with potentially more to come.

Or, if you’re considering buying, particularly as an investor, it could be worth looking at one of these hotspot cities – even if you don’t live there yourself.

No matter where you plan to buy, understanding your borrowing power is a key starting point.

Give us a call today to find out how much you can borrow and what grants and schemes you might be eligible for to help fund your next purchase.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Not sure what refinancing is all about? You’re not alone. Our quick explainer lets you master the basics and helps you work out how much you could save.

Home loan refinancing is a hot topic right now.

Ever since interest rates hit an upward trajectory in May 2022, skyrocketing numbers of homeowners – as many as 28,000 each month – have turned their attention to refinancing.

However, plenty of Australians could be missing out on the savings of refinancing simply because they’re unsure of what’s involved.

Research by Finder shows one-in-five people are in the dark about refinancing, while 63% admit to being only “slightly confident” in their knowledge of refinancing.

So, let’s take a quick look at what refinancing is, and how it can reduce stress by potentially putting cash back in your pocket.

Refinancing simply means replacing your old mortgage with a new loan and lender.

The process is similar to the one you followed to apply for your current loan.

You decide the loan you’d like to switch to, make a formal application, and provide evidence of income, expenses, and your personal ID.

If the loan is approved, you can sit back and relax as the new lender arranges to pay out your old loan. When that’s taken care of, you just start making repayments to the new bank.

Refinancing can be a surprisingly simple process. Better still, it can all happen very quickly, usually taking about four weeks from start to finish.

Refinancing can be an opportunity to access home equity, enjoy better loan features, or consolidate several personal debts.

But the number one reason for refinancing is to save money by paying a lower loan interest rate. Those savings can help take the financial pressure off homeowners.

According to Finder, 60% of refinancers admitted to being stressed about their home loan before deciding to switch.

If that sounds like you, making the move to a new loan could be a valuable stress buster.

Potentially, a lot!

That’s because lenders are still saving their best deals for new customers.

The average rate on established loans is currently 6.20%. But if you’re a new customer, you’re more likely to pay an average rate of 5.99%.

That’s an instant saving of 0.21% interest. Think of it as reversing almost one official rate hike.

So what does that rate difference mean for your hip pocket?

Right now, the average loan being refinanced is worth $526,093. On that balance, a 0.21% rate saving could slash more than $70 off each monthly repayment, which equates to $840 in the first year alone, assuming a 30-year loan term.

If you’re starting to feel the interest rate squeeze, give us a call today to discuss your refinancing options.

We’ll help you work out if refinancing is the right step for you and how much you could save by switching to a new loan and lender.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Know anyone who wants to buy their first home? A new report confirms that low deposit schemes are getting younger buyers into a place of their own sooner.

First home buyers are ignoring headlines warning that it can take years to save a deposit.

Instead, they’re flocking to guarantee schemes that allow them to get into the market with just a 5% deposit – and without the cost of lenders’ mortgage insurance (LMI).

NHFIC, which runs the First Home Guarantee schemes set up by the federal government, says that in 2022/23, close to one-in-three first home buyers tapped into the guarantee schemes.

That’s up from one in seven the year before.

In total, 41,700 home buyers got into the market with the help of guarantee schemes last financial year, following an uptick in the number of places available.

What’s especially exciting about NFHIC’s research is that it shows the schemes are allowing younger buyers to crack the property market.

In 2022/23, more than half of all places in the First Home Guarantee and Regional First Home Buyer Guarantee were taken up by people under the age of 30.

There has also been a fivefold increase in the number of buyers aged 18-24.

The low deposit schemes are also helping a growing number of key workers such as teachers, nurses and social workers purchase a home.

Around 7,721 guarantees were issued to key workers last financial year. Great news for these essential workers in our community!

The First Home Guarantee has at times attracted criticism. This has largely been around the risks of buying with just a 5% deposit, which can mean taking on a larger loan with higher repayments.

But NFHIC data suggests this hasn’t been a problem.

Fewer than 0.1% of homeowners using the schemes have fallen behind on their loan repayments, which is less than the market average for all buyers with a low deposit loan.

Better still, close to 10,000 scheme borrowers (over 12% of total guarantees issued to date) have already transitioned out of the scheme, with most of these buyers having accumulated enough equity to achieve a loan-to-value ratio (LVR) of less than 80%.

If you’re a first home buyer struggling to save a 20% deposit, it’s good to know there is a pathway to home ownership that can get you into a place of your own sooner.

And it can also help you to avoid paying LMI – which can cost you anywhere between $4,000 and $35,000, depending on the property price and your deposit amount.

Conditions apply for the 5% deposit schemes, but new rules mean you can buy with a sibling or mate and still be eligible for this valuable financial helping hand.

With property values rising in many markets across Australia, time is of the essence.

Call us today to see if you can buy a home with a 5% deposit and zero LMI.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Property prices have soared almost 7% this year alone. With the upswing predicted to continue, we unpack what’s driving national housing values higher – and why it could pay to get into the market sooner.

Another month, another round of price upticks.

September marked the eighth consecutive month of home price growth, with CoreLogic saying property values nationally are up 6.6% since January.

That’s a solid price hike. The crazy thing is that prices are soaring despite a whole slew of interest rate hikes over the past 18 months.

The key factor putting a rocket under property prices is a shortage of homes listed for sale.

Homeowners are sitting tight rather than selling across a number of cities, and that’s increasing competition between buyers.

According to CoreLogic, Adelaide, Brisbane and Perth have particularly low levels of homes for sale – around 40% less than previous 5-year averages.

There’s a bit more choice for buyers in Sydney and Melbourne, but both cities are still recording housing price gains (Sydney in particular).

That’s because rising prices aren’t just about a lack of homes listed for sale.

Record levels of net overseas migration are also a contributing factor.

In the year to March 2023, net overseas migration added 454,400 people to our population. That’s an extra 1,245 people each day, all looking for a home.

And according to ABS data, most immigrants settle in Sydney and Melbourne.

So as you can see, despite high interest rates, there’s upward pricing pressure on the nation’s five biggest capital cities (Hobart, Darwin and Canberra meanwhile have all seen house prices drop over the past 12 months).

At the current rate of growth, CoreLogic predicts we could see national housing values reach new highs as early as November.

Already, homes in Perth and Adelaide have smashed previous price records, notching up median values of $618,363 and $691,591 respectively in September.

Brisbane homes look set to reach record values in October, with the city’s current median home value ($761,379) just 0.6% below the previous peak.

As home prices nudge towards new highs, PropTrack says last year’s price falls have been completely reversed.

And most of the data suggests that prices are unlikely to take a tumble any time soon.

That’s because it’s possible that interest rates have peaked, population growth is rebounding strongly, and there is a shortage of new home builds.

Already we’re seeing a surge in home loan applications as more Australians recognise the current market provides a window of opportunity to buy before values rise higher.

No matter whether you’re buying a first home, second home or investment property, buying today could help you beat future price hikes.

So if you’ve got your eye on the property market, call us today and we can help you assess your borrowing power in the current climate, and even help line you up with pre-approval so you’re ready to strike when the opportunity arises.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Apartments stand out as an affordable choice when it comes to cracking the property market, not to mention downsizing. But a looming shortage may soon push unit values higher.

For many of us, buying a house on its own block of land is the ‘great Australian dream’.

While plenty of people achieve this goal, our property journey is often book-ended by apartment living.

For first home buyers, units can be an affordable choice, costing around 30% less than houses according to CoreLogic.

Then, as we head into our senior years, an apartment offers secure, low-maintenance living, often with a wealth of amenities right on the doorstep.

Apartments may be affordable today, but a lack of new apartment construction, coupled with rising immigration levels, points to a looming apartment shortage according to CoreLogic.

And that could push values higher.

Over the next few years, new apartment construction is forecast to be 40% lower in the 2010s, leading to a shortfall of over 100,000 homes by 2027.

Close to 60% of the new home shortfall is expected to be in the apartment market.

On the demand side, CoreLogic says a stronger-than-expected level of migration into Australia has seen overall housing demand “skyrocket”.

Historically, new migrants head to the high-density areas of our big cities, putting extra pressure on the unit market.

As CoreLogic explains, with interest rates potentially easing in 2024, greater demand and tight supply could fuel a “price boom” in the unit market.

Modern apartments are packed with the latest design and sustainability features, meaning they are no longer the poor relation of freestanding houses.

Across our major cities, apartments now account for 30% of all homes, up from 23% in 2010.

And the appeal doesn’t just lie with affordability.

Today’s apartments usually come with a wealth of benefits, including:

Government schemes: because apartments are generally cheaper than houses, they’re more often under the price caps for a range of government schemes, including the Home Guarantee Scheme, stamp duty concessions, and first home owner grants (usually for new builds). These schemes can be combined to potentially save you tens of thousands of dollars and get you into the property market years sooner.

Sought-after locations: apartment living can be the difference between living close to work, or facing a long daily commute from the outer suburbs.

Lifestyle advantages: the days of apartments being cramped and lacklustre are over. A variety of on-site amenities, from barbecue areas to pools, gyms and car-wash bays, make unit living convenient and relaxing.

Low maintenance living: not interested in spending precious spare time mowing the lawns or cleaning the gutters? It turns out plenty of others aren’t either. Unlike houses, units require minimal upkeep, letting residents enjoy more quality time.

Improved security: if you’re after a lock-and-leave lifestyle, modern apartments fit the bill. Advanced security features add up to a safe and secure living environment.

Right now, apartments still present an affordable option for first-home buyers, downsizers and investors.

The median apartment price across our state capitals is currently $637,593 – but if CoreLogic is correct, that figure could soon increase as demand outstrips supply.

So if you’d like help exploring your options to purchase your first property – for example, with just a 5% deposit via the Home Guarantee Scheme – then get in touch today to discover your borrowing power.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

There’s a lot to be said for having your home loan pre-approved. But does pre-approval mean you’re putting the cart before the horse? Definitely not. Here are three ways pre-approval can help you get ahead of the competition.

Here’s a handy tip: you don’t have to wait until you’ve found a home you’d like to buy before making mortgage enquiries with a lender.

It’s possible to have a home loan pre-approved before you’ve even started to wear out shoe leather at open home inspections.

It can mean you’re ready to go with your loan, with only a few formalities to sort out, as soon as you’ve found the right place.

Even better, pre-approval doesn’t mean you’re committed to taking out a loan. It’s not a problem if you have a change of plans.

Here are three ways home loan pre-approval can put you in front in today’s market.

When it comes to a major step like buying a home, there’s no room for guesswork.

With a pre-approved home loan, you know exactly how much you can borrow, and that’s the foundation for your home-buying budget.

It means you can focus on homes within your price range, and make an offer with confidence.

Pre-approval is especially important if you plan to bid at auction. It sets a clear line in the sand for your highest bid.

In today’s market, homes are selling in turbo-charged timeframes.

Figures from CoreLogic show the median selling time across our capital cities is just 27 days. That’s less than a month!

So you need to act fast to avoid missing out. Sellers might not wait around while you head to the bank to see if you qualify for a home loan.

Having pre-approval in place means you can get the ball rolling as soon as you find the right home, without getting pipped by a more organised buyer.

Nothing says ‘genuine buyer’ like home loan pre-approval.

Don’t be shy about letting real estate agents know your loan is pre-approved. It adds clout to your negotiations and gives vendors confidence that you have the finance to follow up any offer you make.

Just consider keeping some information up your sleeve, such as how much you’ve been pre-approved for.

After all, the real estate agent’s goal is to get the best price for the vendor, not the buyer!

Home loan pre-approval is not a guarantee that you’ll get a home loan.

You won’t get the green light for sure until you’ve found a place to buy, and the bank has checked that the property meets their lending criteria.

Your lender will also want to see that your personal finances haven’t changed since your loan was pre-approved.

It’s also worth keeping in mind that while there aren’t many downsides to obtaining a single pre-approval, getting too many over a short period of time with multiple lenders can potentially negatively impact your credit score and ability to take out a loan – as lenders might suspect you’re financially unstable.

Home buyers are often surprised to learn that pre-approval isn’t available with every lender.

Even among banks that do offer this service, not all pre-approvals work the same. One sort is especially worth aiming for.

You may come across two types of pre-approvals:

1. System-generated pre-approvals

This sort of pre-approval is generated by a lender’s computer based on the information you enter about yourself.

You can get a result quickly this way. The catch is that the analysis isn’t thorough, making the outcome unreliable.

In particular, if any of the details you enter are incorrect, the bank’s IT system may wrongly say you don’t qualify for a home loan.

2. Fully assessed pre-approvals

As the name suggests, this type of pre-approval involves your bank’s credit team taking a close look at your finances, credit score and other personal and financial details to be sure you can comfortably manage a home loan.

A full assessment takes more time, but it’s worth the wait. It can help you feel more confident that you’ll be offered a home loan when you find your ideal property.

If you’re looking to buy a home and want to get an edge over the competition (to put in an early offer, for example), then pre-approval might be a much-needed ace up your sleeve.

We can help you work out which lender and which loan product is a good fit for your pre-approval situation.

So call us today to take the guesswork out of home loan pre-approval, and give yourself a head start over other buyers in the market.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

The property market has thumbed its nose at higher interest rates, with values rising almost 5% since March. Here’s why national housing prices are climbing higher.

Australia’s housing market is making a bigger comeback than Barbie.

Despite interest rates rising 4% in a year and a cost of living crunch, home values have skyrocketed with prices soaring 4.9% nationally since March 2023.

The strength of the rebound has wiped out about half the losses recorded in the downturn between April 2022 and February 2023, when home values fell 9.1%.

In fact, the value of Australia’s housing market just hit $10 trillion again – the first time the total estimated value hit double digits since June 2022.

CoreLogic says three factors are pushing up property values:

– Net overseas migration: more people are arriving from overseas than are leaving. That’s a lot of extra people looking for a place to live.

– Use of savings, profit and equity: upgraders are using savings, equity or profits from their home to buy their next place instead of borrowing more. This has seen demand for property stay strong even though rates have climbed higher.

– Tight supply: the volume of homes listed for sale is a lot lower than in previous years. That spells competition between buyers, which is putting pressure on prices.

Home values have been rising steadily over the past six months. What happens from here hinges on how interest rates move, and whether the economy stays in good shape.

As a guide, CoreLogic is expecting some heat to come out of the market recovery by the end of 2023.

That’s great news for home buyers – as long as cooler prices aren’t the result of more rate hikes or a sluggish economy.

In today’s environment of rapidly rising home values, home buyers can score a winning edge by having their ducks in a row before inspecting homes listed for sale.

This increasing need to be organised is one of the key reasons why 67% of Australians turn to a mortgage broker for expert support when they buy their home.

And according to research by Helia, prospective home buyers are getting support in the areas of:

– determining their borrowing power – 63% of those surveyed;

– help choosing the right loan – 60%;

– getting a home loan pre-approved – 56%; and

– applying for a loan – 55%.

So if you’d like help in any of these areas, or you want to get into the market before prices rise further, call us today to explore your home loan options.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

No change to the cash rate again this month, but lenders’ mortgage rates have been jumping around more than a bunch of toddlers at a Wiggles concert. We reveal the current average rates to see how your loan compares.

Home owners are celebrating the official cash rate staying on hold for several months. But behind the scenes, Mozo reports that lenders have been “astonishingly busy” adjusting their home loan rates – both up and down.

Key movements over the last month include NAB, CommBank and Bank of Queensland lifting some of their variable rates.

However, in the fixed rate market, plenty of lenders including big banks such as CommBank, ING and Macquarie have slashed their fixed rates.

It goes to show, you can’t assume your home loan still offers a competitive rate just because the official cash rate hasn’t budged.

Question is, how does your loan shape up against the market?

Across owner-occupied home loans, the average variable rate right now is 6.60%.

Remember though, this is an average. It can be possible to pay far less.

We are still seeing home loan rates starting with a ‘5’ rather than a ‘6’. This makes it worth checking to see what you’re currently paying.

As of early September, fixed rates are averaging:

– 6.36% – one year

– 6.57% – two years

– 6.60% – three years

If you’re bold enough to fix for five years, the average rate is currently 6.49%.

These fixed rates assume a $400,000 loan with a 20% deposit, meaning a loan-to-value ratio (LVR) of 80%.

It’s the question everyone is asking: when will interest rates start to fall?

First the good news.

A number of banks, including ANZ and Westpac, are tipping the cash rate has peaked and could stay the same for some time.

Westpac thinks we could see the cash rate fall by September 2024. AMP meanwhile is forecasting rate cuts even sooner.

But … not everyone agrees.

NAB economists expect one more rate hike before the end of 2023, with rates likely to fall by next Spring.

And the Reserve Bank of Australia (RBA), which makes the official rate calls, is warning we could see more rate hikes depending on how inflation and the economy are tracking.

Even the experts can’t agree on where rates are heading.

But the banks aren’t waiting around for the RBA to drive their rate decisions, and neither should you.

Call us today to see how your home loan rate compares to the broader market. Chances are there’s a better deal out there just waiting to be claimed.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

The start of a new year is a great time to sit back, take stock of your financial situation and plan for the year ahead.

As accountants, we love End of Financial Year (EOFY), so put on your accountant hat and do a quick FINANCIAL EOFY REVIEW of your position, with some helpful hints from us.

We all know that keeping track of expenses and receipts is essential for getting the best tax outcome for ourselves and our businesses. So, let’s start the new year off on the right foot by getting organised and keeping track of those expenses and receipts. Excel is a tried-and-true option, but there are also a number of other software solutions that can make this process easier for you. If you are using Xero, take advantage of Hubdoc, a receipt processing software which is free with your Xero subscription. Hubdoc allows you to scan and upload your receipts directly to Xero, making it even easier to keep track of your receipts.

Getting the right structure for your business and investment assets is one of the most important investments you can make in your financial future. The right structure will deliver you the most optimal (read lowest) tax outcome this year and in future years to come.

The right structure will also ensure your assets are protected and that these hard fought for assets are not lost due to unforeseen circumstances, such as business failures, bankruptcy, or family separations.

For example:

The best way to choose the right structure for your needs is to speak to an accountant or financial planner. If you’re interest in talking about the best structure for you and your personal circumstances, please contact us.

We are talking about the essential, but not so fun types of insurances:

If you already have these types of policies in place and they have been reviewed recently, great work! You’re one step ahead of many people - full points!

if you have these types of policies through your superannuation fund but you haven’t reviewed them to make sure they are going to deliver the financial outcome you and your family need, it’s better than nothing but not ideal - half points!

If you don’t have any of these policies, you should get them in place as soon as possible.

These policies should evolve with you over the course of your life. For example:

Our Financial Planners are able to assist you with your personal insurance needs, even if it is just a general chat to sense check your cover. You will never regret looking into this and ensuring you and your family are taken care of.

A good business can be a valuable asset, but in the event of death or illness of the owners who are instrumental to the operation of the business, the value can quickly be lost, or it can be very hard to extract in a sale situation.

To protect the value of the business, business owners can take out life insurance, TPD insurance and Key Person insurance over owners and key personal to protect the value of the business.

If you have such policies in place, that’s great! But like all things, they need to be reviewed regularly to ensure they are adequate for the current businesses’ needs.

If you are interested in talking about your existing insurances or putting them in place, please contact us.

Let’s be honest, no one likes to think about death, which is very apparent to us as we see too many people who either don’t have a will or have not renewed their estate plan for many years.

You should consider looking into your estate planning if:

Similarly, if you have recently started a business and/or established a company or trust that you control, it is imperative that these changes to your financial structure are dealt with in your will, so it’s time for an update!

If this is something that is keeping you up at night (or maybe it should be), we can refer you to an estate planning lawyer to put in place the appropriate measures to give you peace of mind that your loved ones will be looked after if the worst was to happen to you.

Interest rates have been increasing significantly over the recent months. We are still seeing too many people paying more interest than they should be. This is known as the ‘bank loyalty tax’, which is a term we use to describe the extra interest you pay when you stay with the same lender, even though there may be better rates available elsewhere. We often see people paying up to 1% more than what otherwise may be available.

There are a couple of ways we can help:

If you’re interested in learning more about how we can help you with your loan interest rates, please contact us.

Like everything else it seems at the moment, insurance premiums are skyrocketing. Now is a good a time as any to review your insurance policies to ensure you are not paying more than you need to, and most importantly ensuring you have sufficient cover over your assets if something was to go wrong.

First home buyers who bought into the market using the federal government’s 5% deposit scheme have racked up $82,000 in home equity on average, new data shows.

It’s been three years since the First Home Loan Deposit Scheme was launched, and while it’s known today as the Home Guarantee Scheme (HGS), it’s still helping first home buyers get into the market with just a 5% deposit and no lenders’ mortgage insurance (LMI).

The HGS attracted criticism from some circles – some pundits pointed to the low deposit as a stumbling block that could land homeowners in trouble if property values fell or interest rates rose.

It turns out both have happened, yet first homeowners haven’t let it hold them back.

New data from the National Housing Finance and Investment Corporation (NHFIC), which runs the HGS, shows that first buyers who tapped into the 5% deposit scheme are now sitting on impressive piles of equity.

On average, these first-time homeowners have racked up $82,000 in home equity.

It’s a great result, especially when you consider that the average first home deposit across the scheme was just $35,200 in 2020, rising to $36,400 in mid-2023.

Compare that to the average deposit of $159,000 across the broader first-home buyer market, and it’s easy to see how the 5% deposit scheme gives first-home buyers a valuable leg-up into the market sooner.

Getting a deposit together can be a massive hurdle when buying a home.

Research by Finder shows it can take 12 years for a young Australian to save a deposit for an average-priced apartment, or 16 years to accumulate the deposit for a house.

But if your deposit is lower than 20%, you can get stung with LMI, which can cost you anywhere between $4,000 and $35,000, depending on the property price and your deposit amount.

But through the NHFIC, the federal government has three low deposit, no LMI schemes – all under the HGS umbrella.

The first two, the First Home Guarantee and Regional First Home Buyer Guarantee, support eligible buyers to purchase a home with a low 5% deposit and no LMI.

The Family Home Guarantee, meanwhile, assists eligible single parents and guardians to buy a home with a deposit of just 2% and no LMI.

Along with the HGS, there can be other options such as family pledge loans, or the use of a guarantor, that could slash the time it takes to buy a home of your own.

So if you want to crack the property market sooner rather than later, call us today to find out if you’re eligible to buy a first home with just a 5% deposit.

You could be in a place of your own by Christmas!

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

The highly anticipated Help to Buy Scheme will kick off next year, giving more Aussies a chance to score their dream home. Today we’ll unpack how the new federal government scheme will work, who it’ll benefit, and the fine print you need to know.

A key election promise of the Albanese government, Help to Buy is a shared equity scheme aimed at helping 40,000 low and middle-income earners buy a place of their own (10,000 allocations per year).

The scheme involves the government making an equity contribution worth up to 40% of the value of a new home, or 30% of the value of an established home.

But that doesn’t mean Anthony Albanese will be rocking up unannounced to claim the guest bedroom, as we’ll explain further below.

Homebuyers need a minimum 2% deposit, and must be able to qualify for a home loan with a participating lender to fund the balance of the purchase. No lenders mortgage insurance is payable.